Service Center Accounting: Allocating IT and Facilities Costs DCAA

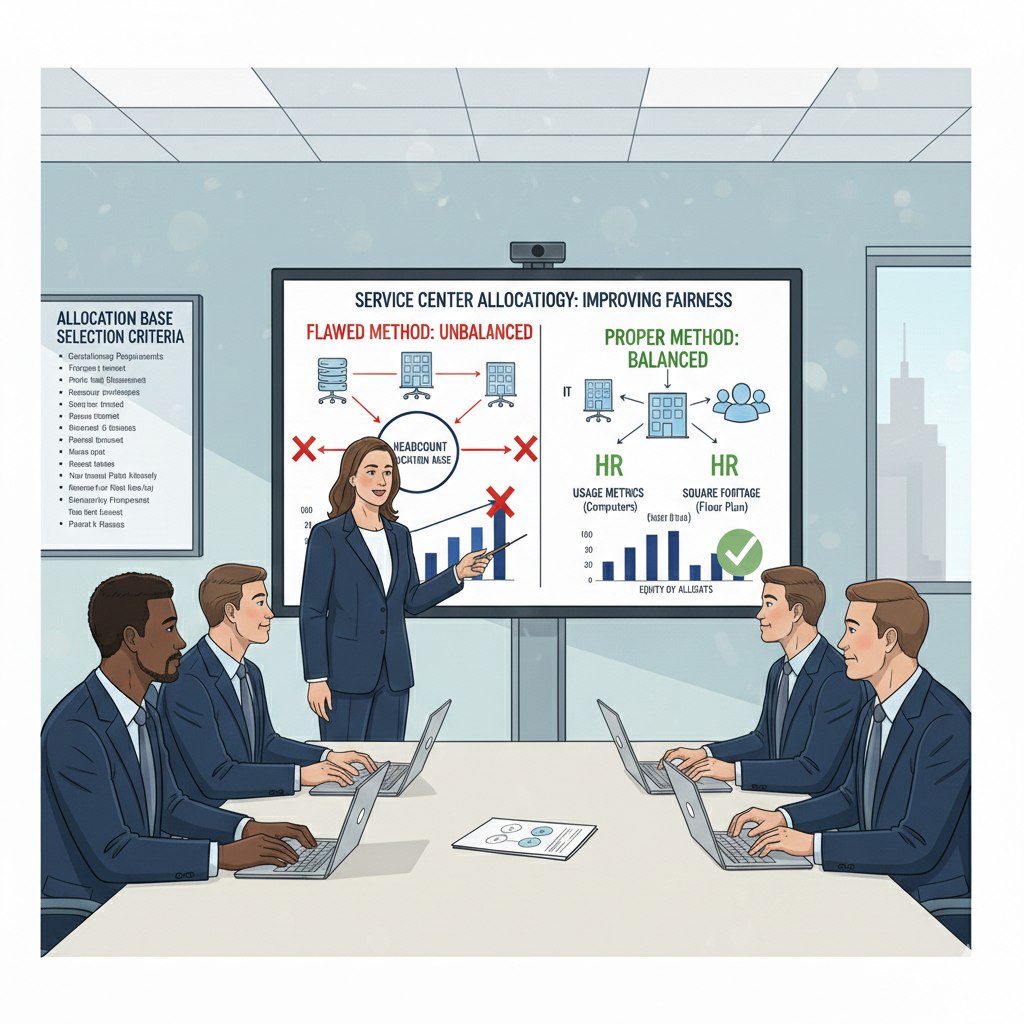

Your company allocated IT department costs using headcount—each employee charged equal share regardless of actual technology consumption—while facilities costs allocated based on direct labor hours even though office space usage had no relationship to project effort. During your accounting system audit, DCAA discovered that your engineering contracts requiring minimal IT resources subsidized administrative operations with heavy system usage, while service contracts performed at customer sites absorbed facility costs for office space those contracts never used. DCAA questioned $215,000 in misallocated service center costs and cited significant deficiencies in allocation methodology lacking causal or beneficial relationships between costs and activities charged. Here’s what contractors miss about service center accounting: IT, facilities, security, HR, and other internal service functions represent legitimate business costs requiring allocation to contracts, but allocation methodologies must reflect actual resource consumption through bases demonstrating causal relationships rather than convenient proxies producing inequitable distribution that overcharges some contracts while undercharging others based on allocation formulas disconnected from reality. Understanding how to establish, operate, and allocate service center costs isn’t about creating accounting complexity—it’s about ensuring shared service costs distribute equitably across benefiting activities through allocation bases measuring actual usage, documenting methodology rationale supporting base selection, and maintaining cost accumulation systems proving service center expenses align with allocated amounts without subsidy or cross-charging errors.

The Legal Framework Governing Service Center Cost Allocation

Federal cost accounting standards establish specific requirements for allocating service center costs ensuring equitable distribution based on measurable benefit or causal relationships. FAR 31.203(c) permits establishing service centers as separate indirect cost pools when costs accumulate for activities benefiting multiple final cost objectives, with service center costs allocated to benefiting cost objectives using allocation bases reflecting relative benefits received. This provision enables contractors to track shared service costs separately from general overhead while requiring allocation methodologies demonstrating that cost distribution reflects actual service consumption rather than arbitrary formulas.

The allocation base selection criteria under FAR 31.203(d) require bases to reflect causal or beneficial relationships between costs accumulated in pools and work receiving allocations. For IT costs, appropriate bases might include computer usage hours, network bandwidth consumption, help desk tickets, or allocated IT staff time depending on what cost drivers best reflect technology resource consumption. For facilities costs, square footage occupied, headcount in space, or dedicated facility assignments provide stronger causal relationships than default direct labor bases that rarely correlate with space utilization. Understanding DCAA compliance requirements means recognizing that base selection requires analysis of actual cost behavior rather than defaulting to convenient proxies lacking demonstrated relationships to costs being allocated.

Cost Accounting Standard 418 governs allocation of direct and indirect costs, establishing that indirect costs must allocate to cost objectives based on beneficial or causal relationship, with allocation bases representing reasonable measures of benefits provided or resources consumed. CAS 418 specifically addresses service center accounting, requiring contractors to establish homogeneous cost pools containing costs of similar activities with comparable relationships to benefiting work, and prohibiting allocation methodologies producing materially inequitable results compared to alternative approaches better reflecting actual resource consumption. When your IT allocation using headcount would produce materially different results than allocation using actual system usage metrics, CAS 418 requires evaluating whether usage-based approach provides more equitable distribution warranting adoption despite administrative complexity.

The critical consideration involves FAR 31.201-4, establishing that costs must be allocable based on relative benefits received or other equitable relationships. Service center costs fail allocability tests when allocation methodologies distribute costs to activities receiving minimal benefits while undercharging heavy consumers, creating the systematic inequity that makes allocations unreasonable regardless of whether total costs charged remain constant. Equitable allocation requires thoughtful base selection, not just mathematical distribution using any available base.

What Contractors Must Understand About Service Center Allocation Challenges

Here’s what contractors miss about service center accounting: establishing separate service center pools doesn’t automatically satisfy compliance—you need allocation bases demonstrating actual consumption patterns and documentation supporting base selection rationale. DCAA compliance explained emphasizes that service center adequacy depends equally on cost accumulation accuracy and allocation methodology equity, with deficiencies in either dimension creating overall service center inadequacy regardless of strengths in other areas.

The allocation base convenience trap emerges when contractors select bases because data is readily available rather than because bases reflect actual causal relationships. This is where audits go sideways—you allocate IT costs using direct labor hours because timekeeping systems already capture those hours, even though technology consumption has no correlation with labor effort on contracts. Your research-intensive contracts with minimal headcount might consume extensive computational resources while labor-intensive service contracts use basic office applications, yet labor-based allocation charges research contracts far less than actual IT consumption warrants. Convenience-driven base selection creates the inequitable allocation that DCAA challenges even when administrative ease provides legitimate operational benefit.

The homogeneity assumption problem surfaces when contractors combine materially different service functions in single pools despite different cost drivers requiring separate treatment. Your “Administrative Services” pool might include IT costs varying with system usage, facilities costs correlating with space occupancy, and HR costs relating to headcount—three distinct cost types with different consumption patterns requiring separate pools and allocation bases for equitable distribution. Combined pooling using blended allocation base produces the cross-subsidization where contracts with high IT usage but low headcount subsidize contracts with opposite consumption patterns, creating systematic inequity that separate pools with appropriate bases would prevent.

The measurement challenge appears when appropriate allocation bases require data not currently captured in accounting or operational systems. Square footage by contract might provide ideal facilities allocation base, but tracking which contracts use which office space requires space assignment records that contractors might not maintain. Computer usage hours by contract could drive IT allocation, but measuring actual usage demands system monitoring capabilities beyond basic network administration. DCAA timekeeping requirements extend conceptually to service center allocation requiring data infrastructure supporting selected methodologies—without measurement capability, optimal bases become theoretical ideals lacking practical implementation feasibility requiring either system investment enabling measurement or alternative base selection using available data with documented rationale explaining compromise.

The direct charging versus service center decision creates classification questions when service functions support specific contracts versus general operations. Your IT staff might include database administrators dedicated to specific contract systems who should charge directly to those contracts, and general network administrators supporting overall infrastructure requiring indirect allocation. Failure to segregate dedicated versus shared service costs creates the direct/indirect misclassification that both undercharges contracts receiving dedicated support (because costs inappropriately treat as indirect) and overcharges contracts receiving only general support (because dedicated costs inappropriately allocate across all work). Proper classification requires evaluating which service costs specifically benefit individual contracts versus providing general support to all operations.

The subsidy and cross-charging risk emerges when service center allocation methodologies systematically overcharge certain contract types while undercharging others, creating pricing distortions affecting competitive positioning. When your firm-fixed-price contracts absorb disproportionate service center costs through allocation bases favoring those contract types, you’re essentially subsidizing cost-reimbursement work where actual costs determine payment regardless of allocation methodology. These cross-subsidies might violate CAS 402 consistency requirements when similar work receives materially different cost treatment based on contract type, customer identity, or pricing arrangements rather than actual resource consumption differences.

The reconciliation and validation gap appears when contractors lack procedures verifying service center costs allocated equal service center costs incurred, or when allocated amounts materially exceed or fall short of actual costs suggesting allocation base errors or pool definition problems. Service center allocation should distribute 100% of accumulated costs to benefiting activities—no more, no less—with significant over/under allocation indicating methodology problems requiring investigation and correction rather than representing acceptable variance within normal accounting tolerances.

Five Essential Steps for Compliant Service Center Accounting

Step 1: Identify and Define Service Center Functions with Clear Scope

Conduct comprehensive analysis identifying which internal support functions operate as service centers providing measurable services to multiple benefiting activities including: information technology (network, systems, help desk, applications), facilities (space, utilities, maintenance, security), human resources (recruiting, benefits, payroll), finance and accounting (AP, AR, cost accounting), and other shared services warranting separate tracking and allocation. For each potential service center, evaluate whether function provides discrete measurable services to identifiable beneficiaries or represents general overhead lacking specific service delivery characteristics.

Develop detailed service center definitions documenting scope including specific activities included, cost types accumulated, services provided, and beneficiaries receiving allocations. Written definitions provide operational guidance for cost classification while supporting audit defense demonstrating systematic approach to service center designation rather than arbitrary pool creation. Include rationale explaining why separate service center treatment produces more equitable allocation than including costs in general overhead pools, with comparative analysis showing allocation differences between approaches.

Establish service center organizational structure and management accountability clearly designating which personnel and functions belong to service centers, implementing management oversight ensuring service center operations serve beneficiaries efficiently, and creating performance metrics measuring service delivery quality and cost effectiveness. Service center management demonstrates organizational commitment to viewing internal services as measurable activities requiring accountability rather than unmanaged overhead consuming resources without visibility or control.

Step 2: Design Allocation Methodologies Reflecting Actual Resource Consumption

Analyze cost behavior for each service center identifying primary cost drivers determining resource consumption and expense levels. For IT centers, drivers might include active users, computational hours, storage consumption, network bandwidth, or support tickets. For facilities, drivers could include square footage occupied, headcount in space, dedicated equipment usage, or utilities consumption. This driver analysis identifies potential allocation bases demonstrating causal relationships with costs being allocated rather than relying on default proxies lacking demonstrated correlation.

Evaluate alternative allocation bases comparing multiple candidates for each service center against criteria including: causal relationship strength between base and costs, measurability using available or obtainable data, stability preventing excessive allocation fluctuation, and administrative feasibility enabling practical implementation without excessive cost or complexity. Select bases providing optimal balance between equity and practicality, recognizing that theoretically ideal bases might prove impractical while convenient bases might lack sufficient causal relationship warranting compromise selection with documented rationale.

Document allocation methodology rationale explaining selected bases, comparing alternatives considered, demonstrating why chosen approaches produce more equitable allocation than alternatives, and describing measurement procedures ensuring base accuracy. This documentation supports both internal methodology understanding and external audit defense, demonstrating deliberate design rather than arbitrary selection or unexamined convention. Include periodic review procedures ensuring methodologies remain appropriate as business operations, technology, or service center functions evolve requiring updated treatment.

Step 3: Implement Cost Accumulation and Measurement Systems

Configure accounting systems with dedicated general ledger accounts for each service center enabling clear cost accumulation separate from general overhead pools. Establish account structures capturing service center costs by type (labor, materials, equipment, facilities) supporting cost analysis and management control while enabling verification that accumulated costs match allocated amounts. Service center account detail provides transparency about cost composition and trends that aggregated overhead pools cannot offer.

Deploy allocation base measurement systems capturing data required for selected methodologies including: timekeeping for labor-based allocations showing service center staff time distribution, IT systems monitoring usage metrics when technology consumption drives allocation, facilities management tracking space assignments and occupancy, and operational systems recording service delivery metrics like tickets processed or transactions completed. Measurement system accuracy determines allocation reliability, with inadequate measurement undermining even well-designed methodologies through unreliable base data.

Establish service center billing or allocation procedures distributing costs to beneficiaries based on measured consumption and documented rates, with allocation processing frequency matching business cycle needs (monthly for management visibility, quarterly for rate stability, annually for simplicity). Implement allocation documentation showing bases used, rates calculated, and amounts charged to each beneficiary, creating audit trail supporting verification that allocation processing followed documented methodology without unauthorized adjustments or errors.

Step 4: Prevent Common Service Center Accounting Errors

Implement controls preventing direct charging of service center labor to contracts except when personnel perform contract-specific work justifying direct classification. Service center staff generally charge time to service center accounts creating indirect costs for subsequent allocation rather than charging directly to contracts, with direct charging limited to extraordinary situations where personnel temporarily perform contract work outside normal service center functions. This segregation maintains service center cost accumulation integrity while preventing the direct/indirect classification errors that undermine allocation methodology.

Establish double-counting prevention procedures ensuring service center costs don’t simultaneously appear in both service center pools and general overhead or G&A pools. When IT costs accumulate in IT service center, those costs must exclude from overhead pools to prevent duplicate allocation through both service center rates and overhead rates. Clear pool boundaries with documented cost classification rules prevent the overlap creating double-counting that CAS 418 prohibits.

Deploy service center reconciliation procedures verifying total costs allocated equal total costs accumulated in service center pools, investigating significant variances suggesting allocation base errors, measurement problems, or pool definition issues. Service center allocation should distribute 100% of costs to beneficiaries with only minor variances from rounding or timing differences, while material over/under allocation indicates methodology problems requiring investigation rather than representing acceptable accounting variance.

Step 5: Maintain Documentation Supporting Methodology and Allocation Accuracy

Develop comprehensive service center accounting manual documenting pool definitions, allocation base selections, measurement procedures, rate calculations, allocation methods, and controls preventing common errors. This manual provides operational reference for accounting staff while supporting audit verification enabling DCAA understanding of methodology without extensive questioning. Include visual aids like cost flow diagrams showing how costs accumulate in service centers and allocate to beneficiaries through documented bases and rates.

Create detailed allocation calculation workpapers showing service center cost accumulation by type, allocation base measurement and totals, rate calculations dividing costs by bases, and allocation distribution showing amounts charged to each beneficiary. Workpaper quality determines audit efficiency, with well-organized documentation enabling rapid verification while inadequate support necessitates extensive additional requests prolonging audits and increasing questioned cost risk when supporting detail cannot be produced.

Implement periodic methodology review evaluating service center allocation effectiveness through: beneficiary feedback about allocation equity and whether charges reflect actual consumption, comparative analysis examining whether alternative bases would produce materially different allocations suggesting current methodology inadequacy, and management assessment determining whether service center structure supports operational objectives including cost visibility, accountability, and resource management. Systematic review prevents methodology stagnation maintaining legacy approaches despite business evolution requiring updated treatment.

The Investment in Service Center Accounting Excellence

Implementing compliant service center accounting costs between $15,000 and $50,000 for small to mid-sized contractors including service center design, allocation methodology development, system configuration, documentation preparation, and training. Annual maintenance costs typically run $5,000 to $15,000 for ongoing allocation processing, methodology monitoring, and documentation updates. These investments enable equitable cost allocation while providing operational visibility into shared service costs supporting management decisions.

Let me show you the value: contractors with proper service center accounting allocate shared costs equitably based on actual consumption preventing systematic over/undercharging of contracts, gain operational insights from service center cost tracking enabling informed decisions about outsourcing, technology investment, or facility utilization, and demonstrate cost accounting sophistication that DCAA recognizes through efficient audits. They avoid the substantial questioned costs from inequitable allocation methodologies systematically mischarging contracts based on flawed bases.

Contractors with inadequate service center accounting face questioned costs when DCAA determines allocation bases lack causal relationships producing systematic inequity, miss operational improvement opportunities that service center visibility would reveal about resource consumption patterns and efficiency, and experience pricing disadvantages when flawed allocation methodologies distort true costs of different work types affecting competitive positioning. They discover that ignoring service center accounting creates both compliance risks and missed management opportunities.

Understanding Service Center Requirements Across Contract Types

Service center accounting requirements apply when contractors maintain cost-reimbursement or time-and-materials contracts where indirect cost allocation directly affects billing, though benefits extend to fixed-price contracts requiring accurate cost understanding for proposal development and profitability analysis. FAR cost principles and CAS standards governing service center allocation apply uniformly across Department of Defense, NASA, Department of Energy, and civilian agency contracts, meaning methodology must satisfy consistent standards regardless of customer.

CAS applicability depends on contract size thresholds and contractor revenue, with CAS-covered contractors subject to specific service center requirements in CAS 418 while non-CAS contractors follow FAR principles establishing similar equity expectations through different regulatory frameworks. Understanding your CAS status determines specific compliance obligations while recognizing equitable allocation remains fundamental requirement regardless of formal coverage.

Your Path to Service Center Accounting Success

The service center accounting landscape rewards contractors who invest in thoughtful methodology design, allocation base analysis, and comprehensive documentation rather than defaulting to convenient bases lacking causal relationships. DCAA evaluates service center allocation through base appropriateness assessment and equity analysis, with adequacy depending on demonstrated relationships between costs and allocation rather than mathematical distribution using any available base.

For contractors seeking service center compliance, Hour Timesheet provides labor tracking supporting various allocation methodologies including service center staff time distribution, direct labor bases for service allocation, and detailed project charging supporting consumption-based allocation bases. Our systems provide data accuracy that service center allocation demands.

Your shared service costs deserve allocation methodology reflecting actual consumption patterns through bases demonstrating causal relationships. Invest in service center accounting producing equitable distribution while enabling operational insights supporting business decisions.